Raising money as new private equity (PE) fund manager can be daunting. I’ve distilled the necessary steps into the following checklist, which should help you develop a compelling investment case for prospective investors.

PE Fundraising Checklist

Private equity investors, also known as limited partners (LPs), usually see hundreds of funds but only invest in a handful of them. To cut, it is essential to consider all four of these points together to give a convincing case to the inevitable question of “why should we invest in you?”

✅ Budget the fund size and fees necessary to execute the strategy.

✅ Finalize a legal structure that provides potential flexibility down the road.

✅ Compile investor lists and separate them into buckets based on long-term capital allocation goals.

✅ Prepare for the marketing phase with clear return targets and benchmark metrics.

1. Fund Size and Fees

The size of your fund needs to accommodate your strategy. You need to consider the market map for potential portfolio companies, the required investment size, and the number of investing partners. It always looks better to set a conservative fund size, be oversubscribed, and raise the target than coming short of your round adjective and taking longer to close. However, LPs will insist on a hard cap close to the target to ensure that you close up fundraising fast and get to investing. LPs also want to control for the alpha decay that comes with larger AUMs due to inefficient deployment of funds on “next best” ideas.

How Competitive Are Your Fees and Terms?

The most effective strategy for first-time fund managers is offering LP-friendly terms. The management fee should be reasonable (around 2%) and reduced after the investment period. In addition, the fund should use a European carry mechanism that calculates carried interest on a whole fund basis. Finally, a significant portion of your wealth should be committed to the fund. After creating a more developed track record, your fund can slowly adopt GP-friendly terms, but being LP-friendly at the beginning increases your success rate during the first fundraising.

What Is Your “Sweet Spot”?

As fund size increases, generated alpha can increase at first due to increased buying power and resources necessary to compete for bids. However, beyond a certain point, AUM growth translates to inefficient capital deployment and a deteriorating track record. The resulting revenue will be impacted through two different channels:

The management fee channel. Revenue grows with AUM because of a fixed management fee charged on committed capital during the investment period and adjusted to cost during the harvesting period.

The performance fee channel. Performance revenue is a factor of capital deployed and realised alpha per unit of deployed capital. Recognised alpha per unit of deployed capital generally refers to the best ideas mentioned earlier, but total performance revenue is growing. This illustrates a misalignment of incentives between GPs and LPs and explains the prevalence of hard caps.

A long-term view prioritising LP relationship preservation will guide your fund size.

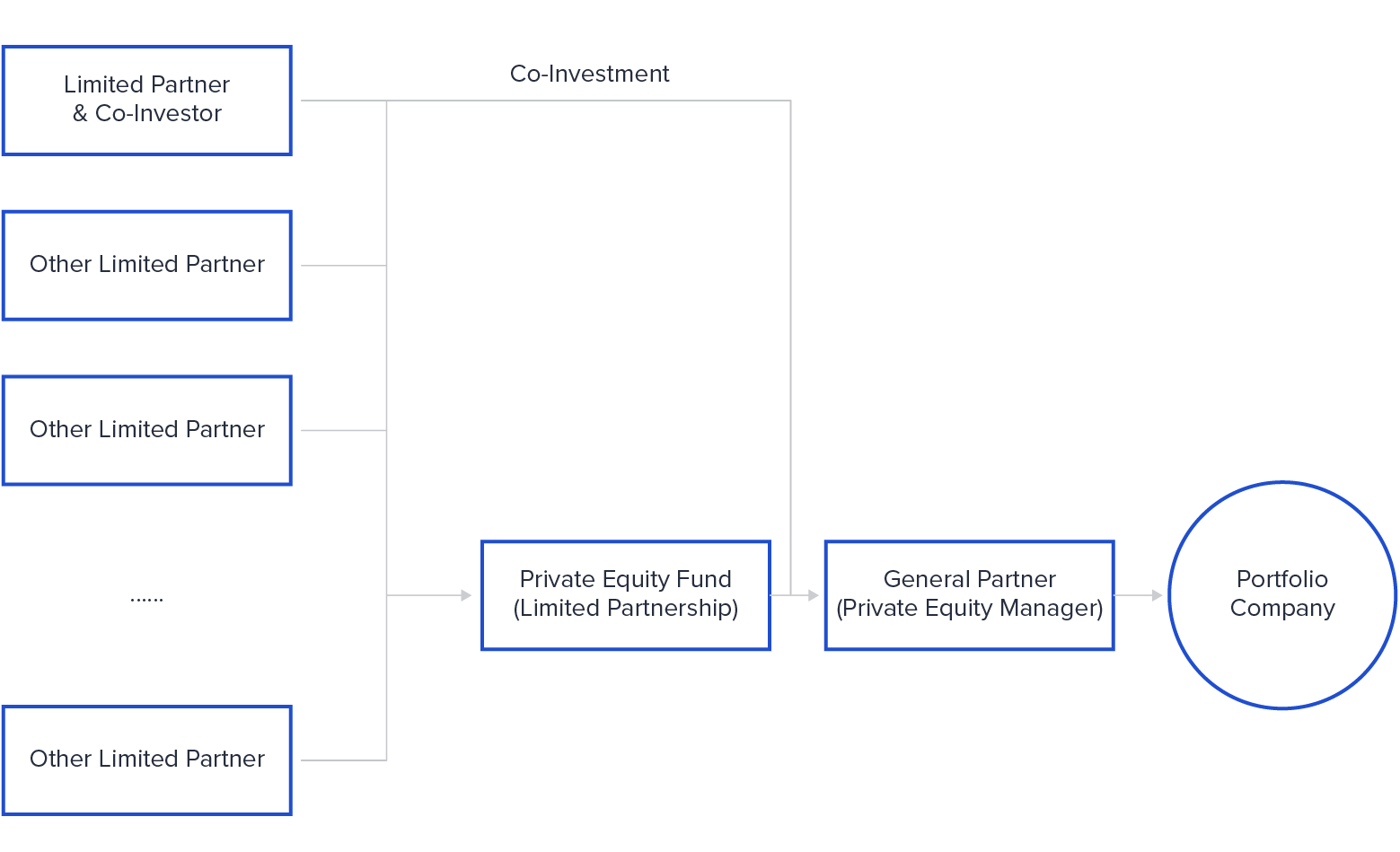

2. Using Co-investments as an LP Magnet

Consideration of the legal structure of your fund can provide flexibility to “draft” in prospective LPs later on by initially engaging with them as co-investors. Many LPs seek co-investment opportunities to achieve higher net returns, efficiently control capital deployment, and have better levers on industry/geography exposure. Co-investments are also an excellent way for LPs to perform ongoing due diligence, especially on new fund managers. On top of this, offering co-investments reduces the blended fee for LPs as no management fee is charged on the co-investment amounts. Co-investments are typically characterized by a shorter duration and predictability of the timing of capital calls.

Co-investments as an LP Magnet

From your perspective, offering co-investments will facilitate access to capital, strengthen relationships with LPs, and manage your fund exposure limits. In a 2015 Preqin survey, 44% of respondents noted that co-investments were a “very important” factor in achieving successful LP solicitations down the line.

3. Appraising the Appropriateness of LPs

Each LP has different concerns, goals, and requirements based on its stakeholders. An LP relationship lasts a minimum of 10 years. While diversifying your LP base can protect you from unexpected dropouts, it is paramount to focus on LPs with the best fit and be aware of your tradeoffs.

LPs can be split into three buckets, determined by their investment characteristics:

Patient Capital

Large institutional investors are insensitive to business cycle swings and can almost always fulfil their capital commitments. Endowments and pensions may hold large amounts of capital to deploy, but they take longer on due diligence and are restricted by strict mandates. Institutional investors will also expect you to accommodate their reporting requirements, which can be onerous and bureaucratic and may, at times, force you to disclose returns metrics publicly.

Flexible Capital

A fund of funds has the workforce and expertise to facilitate a fast due diligence process. However, a fund of funds manager cares more about quick financial returns to make up for their double layer of fees. These funds charge their end investors fees, including their internal operating costs and the fees passed on by the managers of their underlying investments.

Family offices are also more fast-moving than institutional investors, and their investment goals are very varied and can rely on qualitative aspects that are hard to ascertain. Banks and insurance companies are warming up to the idea of riskier investments but are heavily directed by the prevailing economic, regulatory, and stock market conditions.

Value-add Capital

Corporate LPs invest in knowledge transfer opportunities and to find acquisition targets, but they can also assist in winning deals and guidance during the portfolio management phase. Therefore, if you envisage hands-on interventions during the portfolio management phase, a strong corporate investor with potential client leads and synergistic assets can be a unique value-add differentiator when considering your target LP base.

It has become common in recent years for corporations to start their internal investment divisions, forsaking the tradition of mandating external managers to invest their capital. While this trend is set to continue, many corporations still prefer specialist fund managers' expertise.

Kamal Rastogi is a serial IT entrepreneur with 25 yrs plus experience. Currently his focus area is Data Science business, ERP Consulting, IT Staffing and Experttal.com (Fastest growing US based platform to hire verified / Risk Compliant Expert IT resources from talent rich countries like India, Romania, Philippines etc...directly). His firms service clients like KPMG, Deloitte, EnY, Samsung, Wipro, NCR Corporation etc in India and USA.